Economics U$A: 21st Century Edition

Stagflation (Macroeconomics)

1970s America saw a new kind of inflation, based on supply and not demand: “stagflation,” caused by Arab oil embargoes and worldwide crop failures. In 1973 President Ford and Fed Chairman Arthur Burns tried to control inflation by choking the money supply. They failed. In the 1990s the U.S. had three ways to ease inflation: Technological innovation, market globalization, and expenditure restraint. Demand management policies fight cost-push inflation only by causing extremely high unemployment, and rising inflation and rising unemployment can parallel each other.

All Video on Demand files are protected by copyright law and are free for this streaming purpose only. Downloading, in whole or in part, is strictly prohibited. Offenders will be subject to civil and/or criminal liability under applicable laws.

Unit Overview

Purpose:

To discuss how rising inflation and rising unemployment can occur simultaneously when there is a supply shock; and how demand-management policies can fight cost-push inflation only by causing extremely high unemployment.

Objectives:

- Inflation can come about because of increases in aggregate demand pressures. This demand-pull inflation can result from expansionary fiscal and monetary policies pushing the economy up to its capacity limits.

- There is general agreement that, in the short run, there is a trade-off between the rate of inflation and the amount of slack in the economy (the unemployment rate). However, the trade-off is much worse when there are supply shocks and when wages are indexed to inflation.

- In the early stages of demand-pull inflation, demand-management policies may be able to reduce inflation without causing unemployment to rise to high levels. But in order to fight inflation that is entrenched (e.g., because of high inflation expectations) or inflation that is due to supply shocks, the government would have to reduce aggregate demand significantly, causing a high level of unemployment.

Meet the Series Experts

Alan Blinder

Member of President Bill Clinton’s Council of Economic Advisers, 1993–1994, and Vice Chairman of the Board of Governors of the Federal Reserve System, 1994–1996. Earlier, he was one of the Congressional Budget Office’s first officials, serving as Deputy Assistant Director in 1975. He teaches at Princeton University as the Gordon S. Rentschler Memorial Professor of Economics and Public Affairs in the Economics Department, and is Vice Chairman of The Observatory Group and Co-Director of Princeton’s Center for Economic Policy Studies. He has authored and co-authored 17 books and is a regular columnist for the Wall Street Journal. He has served as President of the Eastern Economic Association, Vice President of the American Economic Association, and on the boards of the Council on Foreign Relations, the Bretton Woods Committee, and the Bellagio Group. Dr. Blinder received his B.A. from Princeton University, M.Sc. from the London School of Economics, and Ph.D. from the Massachusetts Institute of Technology.

Alice Rivlin

Senior Fellow at the Brookings Institution and Member of President Barack Obama’s 2010 Federal Debt Commission, known for her expertise on fiscal and monetary policy. She was Director of the Congressional Budget Office, Director of the Office of Management and Budget, and Vice Chair of the Federal Reserve Board, 1996–1999. She also served as Chair of the District of Columbia Financial Management Assistance Authority and Welfare Assistant Secretary for Planning and Evaluation at the Department of Health, Education, and Welfare. She received a MacArthur Foundation Fellowship, has taught at Harvard University, George Mason University, and New School University, and has served as President of the American Economic Association. She is a frequent contributor to newspapers, television, and radio and has written many books, including Systematic Thinking for Social Action, Reviving the American Dream, and Beyond the Dot.coms (with Robert Litan). Dr. Rivlin received her B.A. from Bryn Mawr College and Ph.D. in Economics from Radcliffe College (Harvard University).

Paul Volcker

Chairman of the Board of Governors of the Federal Reserve System, 1979–1987, credited with leadership in ending a period of high and rising inflation and restoring a base for sustained growth. Later, he became chairman of the firm of James D. Wolfensohn, Inc., concentrating on investment banking services to domestic and international organizations. He served in the federal government for almost 30 years, in posts that included President of the Federal Reserve Bank of New York and U.S. Treasury Under Secretary for Monetary Affairs, where he developed and implemented Treasury debt management and federal credit policies. In the area of domestic finance, he initiated the auctioning of Treasury bonds, an approach that has become customary in the United States and many other countries. A former chairman of the Trilateral Commission, he serves on many public and private boards, including the Group of Thirty, International House, and the Financial Services Volunteer Corps. He is a member of the Institute for International Economics and an overseer of TIAA-CREF, the leading private retirement system in the United States. He has taught at Princeton University and at the Stern School of Business at New York University. Mr. Volcker received his B.A. from Princeton University and M.A. in Political Economy and Government from Harvard University and did postgraduate work at the London School of Economics.

Stanley Fischer

Governor of the Bank of Israel and former U.S. adviser to Israel’s economic stabilization program. He was Vice President of Development Economics and Chief Economist at the World Bank, 1988–1990; First Deputy Managing Director of the International Monetary Fund, 1994–2001; and then served as Vice Chairman of Citigroup, President of Citigroup International, and Head of the Public Sector Client Group. He is co-author of two popular textbooks on macroeconomics. In 2010, he was declared Central Bank Governor of the Year by Euromoney magazine. Dr. Fischer received his B.Sci. and M.Sci. in Economics from the London School of Economics and his Ph.D. in Economics from the Massachusetts Institute of Technology.

What's your Economics IQ?

Take the Economics USA: Stagflation Quiz.

Quiz Addendum

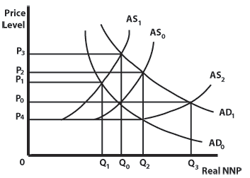

4. Significant increases in price will:

Answer:

shift the aggregate supply curve to AS1.

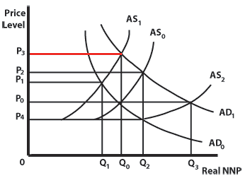

5. The Fed could minimize the impact of price increases on unemployment by increasing the money supply to shift aggregate demand to AD1. In that case the price level would:

Answer:

rise to OP3.

Glossary

- cost-push inflation

Persistently rising general price levels brought about by rising input costs, usually brought about by rising wages, increases in corporate taxes, and imported inflation. - Phillips curve

A curve representing the relationship between the rate of increase in the price level and the level of unemployment. - stagflation

A simultaneous combination of high unemployment and high inflation. - wage and price controls

Limits imposed by the government on the amount by which wages and prices can rise, in order to reduce the inflation rate at a given unemployment rate. - wage rate

The price of labor.