Economics U$A: 21st Century Edition

Monopoly (Microeconomics)

In 1890, the Sherman Anti-Trust Act broke up the monopoly that John D. Rockefeller and his company, Standard Oil, had on the oil industry. In 1914, the federal government was sold on the concept of universal telephone service provided by Ma Bell, a monopoly that was ended by the development of a new technology. In 1998, the U.S. government filed a suit against the world’s largest software company, Microsoft, for participating in anti-competitive practices. These stories explain what monopolies are, and why government sometimes chooses to intervene.

All Video on Demand files are protected by copyright law and are free for this streaming purpose only. Downloading, in whole or in part, is strictly prohibited. Offenders will be subject to civil and/or criminal liability under applicable laws.

Unit Overview

Purpose:

To help viewers understand that the degree to which a firm controls the market affects prices and economic efficiency, and that the government tries to prevent or regulate monopolies.

Objectives:

- Market power is directly related to the producer’s ability to control the total production of a product and therefore keep prices and profits high.

- At one extreme monopolists can control total output and therefore keep prices high—they are the price makers.

- At the other extreme, in perfectly competitive markets, sellers have no control over prices—they are price takers.

- The concentration of market power depends on entry barriers, such as:

- Ownership of a resource (e.g., oil) or process (e.g., patents on Polaroid film) or transportation or marketing outlets.

- Economies of scale (e.g., the large fixed costs necessary to start a telephone company). Some markets, such as those for local utilities, have such large economies of scale that they are “natural monopolies.”

- Even if entry barriers are high, some firms may try to compete with monopolies because the level of the monopolist’s profits is so high.

- The more concentrated market power is in a given market, the higher the likelihood that it is operating in a way that is economically inefficient for society as a whole. Producers with a high degree of market power are likely to set prices at a level that is higher than the level that would prevail in perfectly competitive markets and produce less than would be produced in a perfectly competitive market. From society’s point of view, this is not economically efficient.

- The government tries to minimize or control monopolies:

- If the market is not a natural monopoly, a monopoly may be dismantled by antritrust action.

- In the case of natural monopolies, the government will regulate the firm.

Meet the Series Experts

David Boies

Prominent attorney involved in many high-profile cases, including United States v. Microsoft, during which Bill Gates said that Boies was “out to destroy Microsoft” but the Washington Monthly called him “a latter-day Clarence Darrow.” He also represented Vice President Al Gore in Bush v. Gore; defended CBS in an action brought by General William Westmoreland; defended Napster when the company was sued for copyright infringement; and is representing filmmaker Michael Moore regarding a Treasury Department investigation into Moore’s trip to Cuba while filming for Sicko. Earlier, he was Chief Counsel and Staff Director of the United States Senate Antitrust Subcommittee and served as Chief Counsel and Staff Director of the United States Senate Judiciary Committee. Mr. Boies received his B.S. from Northwestern University and L.L.B. from the Yale Law School.

Henry Geller

Telecommunications attorney and law professor specializing in United States communications policy-making and regulation. He worked at the Federal Communications Commission (FCC) at several intervals from 1949 until 1973, serving as General Counsel and then as Assistant to FCC Chairman Dean Burch. He later served as Administrator of the National Telecommunications and Information Administration during the Carter presidency. He proposed that funds raised from spectrum auctions be dedicated to the development of public broadcasting services, much like the traditional British model of public support for national programming. His contributions to national telecommunications policy led to the National Civil Service Award in 1970. In retirement, he has served as a telecommunications adviser for nongovernmental organizations, including Duke University’s Washington Center for Public Policy Research, the Rand Corporation, and the Markle Foundation. Mr. Geller received his B.S. from the University of Michigan and J.D. from Northwestern Law School.

What's your Economics IQ?

Take the Economics USA: Monopoly Quiz.

Quiz Addendum

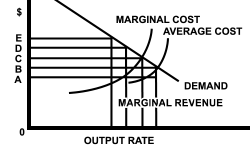

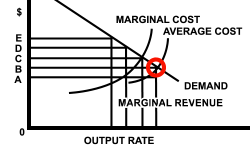

5. The regulatory agency is likely to establish a maximum price of…

Answer:

OB: The commission will set the maximum price at the level where the average cost curve intersects the demand curve.

Glossary

- barriers to entry

Obstacles that make it more difficult for new competitors to enter an area of business, e.g., high start-up costs. - economies of scale

Efficiencies that result from carrying out a process (such as production or sales) on a large scale. - holding companies

Business organizations that allow firms (called “parents”) and their directors to control or influence other firms (called “subsidiaries”). - merger

The combining of two or more companies, generally by offering the stockholders of one company securities in the acquiring company in exchange for the surrender of their stock. - monopoly

A market structure (such as those for public utilities) in which there is only one seller of a product. - monopoly power

A firm’s degree of control over a price for a good. - monopoly profits

Economic gain for a firm that comes as a result of that firm’s control over the market. - natural monopoly

An industry in which the average costs of producing the product reach a minimum at an output rate large enough to satisfy the entire market, so that competition among firms cannot be sustained and one firm becomes a monopolist. - perfect competition

A market structure in which there are many sellers of identical products, no one seller or buyer has control over the price, entry is easy, and resources can switch readily from one use to another. Many agricultural markets have many of the characteristics of perfect competition. - pools

Resources grouped together by companies in an attempt to gain mutual market leverage. - predatory pricing

Setting products at a low price with the intention of driving out competition and preventing new competition. - profit

The difference between a firm’s revenue and its costs. - regulation

Management of an economy by an outside (usually governing) body or set of pre-existing laws. - trusts

A group of companies that illegally work together to reduce competition and control prices.