Economics U$A: 21st Century Edition

Boom and Bust (Macroeconomics)

The nation’s cycles of economic booms and busts were considered intrinsically capitalistic by Joseph Schumpeter who called them “methodic economic growth,” and by Karl Marx who lambasted capitalism as inherently flawed. John Maynard Keynes held that recessions depended on the balance of aggregate demand and aggregate supply. Economist Hyman Minsky provided a promising explanation for the Great Recession of the 21st Century with his theory that the financial system plays a determining role in economic cycles.

All Video on Demand files are protected by copyright law and are free for this streaming purpose only. Downloading, in whole or in part, is strictly prohibited. Offenders will be subject to civil and/or criminal liability under applicable laws.

Unit Overview

Purpose:

To show how successive schools of economic thought struggled unsuccessfully to give a satisfactory explanation of business cycles until John Maynard Keynes showed that shifts in aggregate demand were the primary cause of these fluctuations.

Objectives:

- Classical economists did not have a satisfactory explanation for business cycles. Instead, they viewed them as temporary phenomena brought on by financial panics. They believed that the natural forces in the economy would always bring about an equilibrium between total supply and demand for goods in the economy.

- There were two other more satisfactory explanations of business cycles which provided partial explanations of why the economy could find itself with high levels of unemployment and large inventories of unsold goods.

- Karl Marx provided a theory of mass unemployment in the context of his view of the capitalist system as the exploiter of the working classes.

- Joseph Schumpeter explained business cycles as a natural by-product of growth and innovation. Economic growth, he maintained, resulted in periodic overproduction and subsequent retrenchments.

- It was not until the mid-1930s that John Maynard Keynes developed the concepts necessary to understand how the economy could move toward and remain at a less-than-full-employment equilibrium. One of the key concepts developed by Keynes was aggregate or total demand.

- In very simple terms, aggregate demand is the sum of all the goods and services that buyers are willing to purchase at a given price level.

- Shifts in aggregate demand are affected by the circular flow. The circular flow of income has leakages (savings, taxes, and imports) and injections (investment, government spending, and exports).

- If the amount of leakages equals the amount of injections, then the circular flow (i.e., aggregate demand for GDP/GNP) will remain constant. It will be in equilibrium.

- If the injections are larger than the leakages, aggregate demand for GDP/GNP will grow, and vice versa.

Meet the Series Experts

Paul Samuelson

First American economist to win the Nobel Prize in Economics, cited for doing “more than any other contemporary economist to raise the level of scientific analysis in economic theory.” Economic historian Randall E. Parker called him the “Father of Modern Economics” and the New York Times considered him the “foremost academic economist of the 20th century.” He spent his academic career at Massachusetts Institute of Technology (MIT), where he was awarded MIT’s highest faculty honor, and where he wrote the largest-selling economics textbook of all time: Economics: An Introductory Analysis. He served as an adviser to Presidents John F. Kennedy and Lyndon B. Johnson, and to the United States Treasury, the Bureau of the Budget, and the President’s Council of Economic Advisers. Dr. Samuelson received his B.A. from the University of Chicago and Ph.D. in Economics from Harvard University.

Robert Heilbroner

An economist who regarded himself as a social theorist, integrating disciplines of history, economics, and philosophy. During World War II, he worked at the Office of Price Control under economist John Kenneth Galbraith. After the war, he became a research fellow, then Norman Thomas Professor of Economics at the New School for Social Research. He authored Worldly Philosophers, as well as Economics, the second-best-selling economics textbook of all time. The seventh edition of Economics, published in 1999, included a new final chapter entitled “The End of Worldly Philosophy?” in which he gave a grim view on the current state of economics as well as a hopeful vision for a “reborn worldly philosophy” that incorporated capitalism. Dr. Heilbroner received his B.A. from Harvard University and Ph.D. in Economics from the New School for Social Research.

Willard Thorp

An economist who served as an adviser in domestic and foreign affairs for presidents Franklin D. Roosevelt, Harry S. Truman, and Dwight D. Eisenhower. He helped draft the Marshall Plan and was prominent in business and education. He served as Assistant Secretary of State under Truman for Economic Affairs, 1946–1952. He also served on the U.S. delegation at the Paris Peace Conference of 1946, as a participant in the New York meeting of the Council of Foreign Ministers, and as American representative to the United Nations General Assembly, 1947–1948. Prior to 1946, he worked at the National Bureau of Economic Research, where he compiled centralized data that led to the 1926 publication of Business Annals, a book of economic statistics for 17 countries dating back to 1890. Dr. Thorp received his B.A. from Amherst College, M.A. from the University of Michigan, and Ph.D. in Economics from Columbia University.

Douglas Elliot

Fellow at the Brookings Institution, specializing in the regulation of financial institutions and markets. A financial institutions investment banker for two decades, principally at J.P. Morgan, he was the founder and principal researcher for the Center on Federal Financial Institutions. He has researched financial institutions or worked directly with them as clients in a range of capacities, including as an equities analyst, credit analyst, mergers and acquisitions specialist, relationship officer, and specialist in securitizations. His work encompasses banks, insurers, funds management firms, and other financial institutions. Mr. Elliott received an A.B. in Sociology from Harvard College and an M.A. in Computer Science from Duke University.

Dimitri B. Papadimitriou

Economist and expert on the works of 20th-century economist Hyman P. Minsky, whose alternative theories for why the U.S. economy has periodic booms and busts have gained 21st-century recognition. Papadimitriou has been the Executive Vice President and Provost, Jerome Levy Professor of Economics, and President of the Levy Economics Institute at Bard College. His published works include: Financial Conditions and Macroeconomic Performance: Essays in Honor of Hyman P. Minsky; Hyman P. Minsky’s Induced Investment and Business Cycles; Hyman P. Minsky’s Stabilizing an Unstable Economy; and Hyman P. Minsky’s John Maynard Keynes. Dr. Papadimitriou received his B.A. from Columbia University and Ph.D. in Economics from the New School for Social Research.

What's your Economics IQ?

Take the Economics USA: Boom and Bust Quiz here.

Quiz Addendum

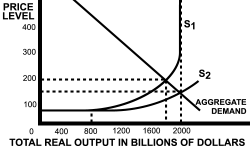

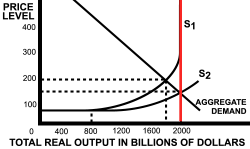

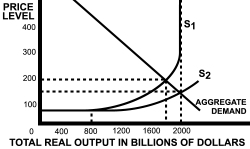

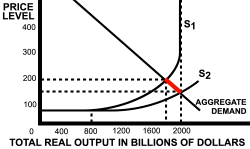

5. If the aggregate supply curve is S1, full employment of the economy’s resources will occur when:

Answer:

total real output is $2,000 billion.

6. If the aggregate supply curve shifts to S2:

Answer:

the demand for money will decrease and interest rates will fall.

Glossary

- aggregate demand curve

A curve, sloping downward to the right, that shows the level of real national output that will be demanded at various economy-wide price levels. - aggregate supply curve

A curve, sloping upward to the right, that shows the level of real national output that will be supplied at various economy-wide price levels. - classical economics

Refers to work done by a group of economists in the eighteenth and nineteenth centuries, emphasizing economic freedom and promoting such ideas as “laissez-faire” and “free competition.” - exports

The goods and services that a country sells to other countries. - government purchases

Federal, state, and local government spending on final goods and services, excluding transfer payments. - imports

The goods and services that a country buys from other countries. - injections

Nonconsumption expenditures on gross domestic product, including investment expenditures, government purchases, and exports. - Keynesians

Economists who share many of the beliefs of John Maynard Keynes. His principal tenet was that a capitalist system does not automatically tend toward a full-employment equilibrium (due in part to the rigidity of wages). Keynesians tend to believe that a free-enterprise economy has weak self-regulating mechanisms that should be supplemented by activist fiscal (and other) policies. - leakages

Nonconsumption uses of income, including saving, taxes, and imports.